Пенсионные налоги и взносы в 2020 году

Обязательные страховые выплаты они же пенсионные налоги и взносы оплачиваются работодателем на каждого своего сотрудника в три внебюджетных фонда: пенсионный, медицинский и социального страхования. Значение подобных выплат заключается в том, что работодатели, включая индивидуальных предпринимателей, таким образом, формируют резерв средств, которые выплачиваются работникам при наступлении страховых случаев, например, больничного или декретного отпуска, а также при выходе на пенсию.

Пенсионные налоги и взносы — виды

Любой работодатель, как бюджетная организация, так и индивидуальный предприниматель, обязан уплачивать четыре вида страховых взносов:

- пенсионный налог или взнос в Пенсионный Фонд России;

- медицинский взнос, который выплачивается в Фонд обязательного мед.страхования;

- обязательный страховой взнос на работников в Фонд обязательного соцстрахования на случай больничных листов и осуществления выплат, связанных с беременностью и рождением детей;

- обязательные взносы в Фонд социального страхования для осуществления выплат, связанных с несчастными случаями и профессиональными заболеваниями.

Налог в пенсионный фонд включает в себя два вида выплат. Одни формируют страховую часть пенсии, вторые – накопительную.

Категории плательщиков обязательных страховых взносов

По закону, обязанность производить выплаты обязательного характера, возлагаются на следующие категории организаций;

- любые организации, начисляющие заработные платы и осуществляющие выплаты наемным работникам – частным гражданам;

- индивидуальные предприниматели, выплачивающие зарплату сотрудникам и наемным рабочим;

- физические лица, не зарегистрированные в качестве предпринимателей, но осуществляющие выплаты зарплаты частным гражданам;

- предприниматели, работающие «на себя», т.е. занимающиеся частной практикой.

На практике случаются ситуации, когда один и тот же субъект экономической деятельности, обязан платить страховые взносы одновременно по нескольким основаниям. Например, налог ИП в пенсионный фонд 2017, если предприниматель трудится «на себя», при этом имеет помощника – штатного сотрудника, то производить оплату он должен и за себя, и за сотрудника.

С чего необходимо платить налог?

Категории выплат, на которые начисляются налоги и страховые взносы – это, прежде всего, оплата труда – зарплаты штатным сотрудникам, выплаты в рамках трудовых договоров и наемным рабочим в рамках подрядных отношений. Если речь идет о штатных сотрудниках, то премии за любой период, отпускные выплаты и компенсации за неиспользованные отпуска – то на все эти виды выплат начисляется налог.

Если речь идет о внештатных сотрудниках, работающих по сделке, временному трудовому договору или в рамках гражданско- правовых трудовых отношений, то все виды выплаченных им вознаграждений за трудовую деятельность также облагаются налогом.

Таким образом, подоходный пенсионный налог взимается со всех выплат в пользу работника – физического лица. Исключения составляют работники, имеющие статус индивидуального предпринимателя. Иными словами, взносы не взимаются, если бюджетное учреждение или предприниматель привлекает к сотрудничеству для выполнения определенного вида работ другого предпринимателя, и оплачивает его услуги.

Кроме того, не происходит начисления на выплаты, которые затрагивают вопросы аренды имущества работника, например, его личного автомобиля.

Взносы в фонды социального страхования обходят стороной сотрудников, работающих в рамках договоров гражданско-правового характера и подряда. Что касается взносов, связанных со страхованием несчастных случаев на производстве, то их оплачивать обязаны организации только в том случае, если о выплатах на случай производственной травмы или ущерба здоровью в ходе выполнения работ, упоминается в самом договоре.

Кроме того, присутствует и единый перечень выплат, в отношении которых действует освобождение от внесения взносов в фонды медицинского и социального страхования, а также не взимается пенсионный взнос. Их перечень приведен в 9 статье 212 федерального закона.

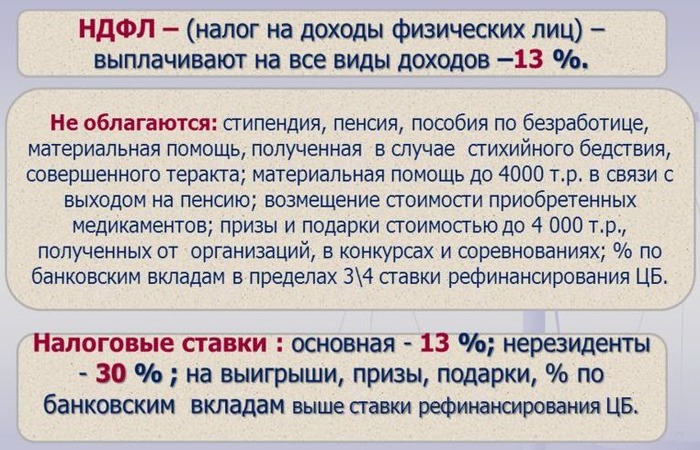

Облагаемая база | ПФР | ФСС | ФОМС | итого |

Не выше предельной величины | 22% | 2.9% | 5.1% | 30% |

Выше предельной величины | 10% | 5.1 | 0 | 15.1% |

Обнаружили ошибку? Выделите ее и нажмите Ctrl + Enter.

Автор: Команда Bankiros.ru

1 496 просмотров20

Расскажите друзьям:Подпишитесь на Bankiros.ru

Предыдущая статья

Пенсионные накопления в 2020 году

Следующая статья

Пенсионные удостоверения в 2020 году

как это происходит в России

Подоходный налог – сумма, выплачиваемая государству с дохода, который получают физические лица на территории страны. По общему правилу на данный момент он составляет 13%.

Подоходный налог – сумма, выплачиваемая государству с дохода, который получают физические лица на территории страны. По общему правилу на данный момент он составляет 13%.

Налог на доходы физических лиц (НДФЛ) – именно таково его правильное наименование, является прямым налогом, который оплачивают не только граждане РФ, но и иностранцы при условии получения какой-либо прибыли на территории страны.

Те из них, которые не являются налоговыми резидентами, обязаны отчислять 30%. При этом НДФЛ берут не с любого дохода, к примеру, не облагаются им социальные выплаты, а в ряде случаев, предусмотренных действующим российским законодательством, предусмотрены так называемые вычеты – уменьшение налоговой базы по определенным основаниям.

Облагается ли пенсия подоходным налогом

По своей сути, пенсия представляет собой социальную выплату, на которую могут рассчитывать граждане, нуждающиеся в особой материальной поддержке. Круг ее получателей довольно широк и это далеко не только лица пожилого возраста. Пенсия выплачивается:

- военным, имеющим определенную выслугу;

- инвалидам;

- несовершеннолетним в связи с потерей кормильца.

Данные социальные выплаты НДФЛ не облагаются.

Однако большинство пенсионеров – лица преклонных лет, достигшие соответствующего возраста и имеющие необходимый трудовой стаж. Как же формируется такая пенсия?

Каждый месяц работодатель платит за каждого работника так называемые страховые взносы. Их сумма составляет определенный процент от заработной платы сотрудника. Часть этих средств идет в ФСС, ФОМС, ТФОМС. Это социальное и медицинское страхование. Большая же часть денежных средств, оплачиваемых работодателем, уходит в ПФР на формирование будущей пенсии сотрудника. Она, в свою очередь, состоит из страховой и накопительной частей.

Справка! Если за наемных работников отчисления производит их работодатель, то лица, занимающиеся предпринимательской деятельностью, платят сами за себя по фиксированным ставкам.

Согласно действующему законодательству, накопительную часть гражданин может оставить в государственном пенсионном фонде, а может выбрать негосударственный пенсионный фонд (НПФ). НПФ предлагают более высокие проценты на эти накопления, поэтому ожидается, что величина пенсии, получаемой через них в будущем, будет выше.

Разобравшись, какие же бывают пенсии и из чего они состоят, можно ответить на вопрос, относительно обложения пенсионных выплат подоходным налогом.

С выплат от государственного фонда НДФЛ не удерживается. Если же пенсия приходит от негосударственного источника, то в таком случае она облагается подоходным налогом. Однако здесь существуют исключения. Так, не платится НДФЛ с пенсий, которые выплачиваются НПФ, имеющими соответствующую лицензию.

Также распространены случаи, когда крупные работодатели самостоятельно заключают договора с выбранными ими НПФ или имеют свой фонд. Их работники по выходе на заслуженный отдых также налог не платят. Иными словами, НДФЛ берется только с только накопительной части пенсии, выплачиваемая НПФ, не имеющим государственной лицензии, с которым работник заключил договор непосредственно от своего имени.

Законодательная база

То правило, что государственные пенсионные выплаты не облагаются налогом, подкреплено п. 2 ст. 217 Налогового Кодекса РФ. Однако эта же норма устанавливает, что подоходный налог берется с добровольного страхования накопительной части пенсии.

Какие налоги платят работающие пенсионеры

В России распространена ситуация, когда многие граждане, имеющие право на пенсию в связи с достижением соответствующего возраста, стараются сохранить прежнее место работы или продолжают трудовую деятельность в другом месте. С точки зрения действующего законодательства никаких препятствий и ограничений для получения пенсионных выплат в таком случае нет. При этом работающие пенсионеры остаются плательщиками различных налоговых сборов.

Так, они уплачивают НДФЛ со своей заработной платы в полном объеме, равно как и остальные граждане страны. Для налоговых резидентов эта сумма составляет 13%.

Также они уплачивают НДФЛ и с других видов доходов, например, выигрышей, дивидендов, от предоставления услуг и продажи товаров и имущества. Облагается налогом и часть пенсии, выплачиваемой по договорам с НПФ, о чем говорилось ранее.

Кроме НДФЛ, существуют и иные, более специфические платежи, обязанность по уплате которых лежит на гражданах. Это имущественный, земельный и транспортный налоги.

Пенсионеры, в том числе и работающие, полностью освобождены от уплаты сбора на имущество.

Важно! Это касается только одного объекта некоммерческой недвижимости. Если у пенсионера их несколько, то льгота распространяется только на один из них по его выбору.

Что касается земельного и транспортного налога, то они относятся к категории местных пошлин. Это означает, что возможность освобождения от них устанавливается на региональном уровне. Таким образом, в части субъектов работающие пенсионеры их платят, а в части нет.

Возврат налога при покупке недвижимости

Налоговый вычет при приобретении недвижимости может получить любой налогоплательщик при условии его официального трудоустройства. Это касается и работающих пенсионеров.

Налоговый вычет при приобретении недвижимости может получить любой налогоплательщик при условии его официального трудоустройства. Это касается и работающих пенсионеров.

Никаких особенностей в порядке его оформления для этой категории граждан нет. Для возвращения налогового вычета пенсионеру необходимо предоставить в ИФНС следующие документы:

- декларацию по форме 3НДФЛ;

- правоустанавливающие бумаги на объект недвижимости;

- справку о сумме ранее уплаченных налогов.

Внимание! Решение по заявлению принимается в течение трех месяцев.

Пенсия, по большей части, является социальной выплатой, которая не облагается налогами. Исключение составляет ее накопительная часть, выплачиваемая НПФ при условии добровольного страхования. Однако обязанность по уплате большинства остальных видов налогов за пенсионерами сохраняется в полном объеме.

Полезное видео

Предлагаем посмотреть видео-сюжет о возврате налога за покупку недвижимости пенсионерами:

15 февраля 2019 12:29

Федеральным законом от 27 ноября 2018 года № 425-ФЗ (далее – Закон № 425-ФЗ) перечень налоговых режимов, поименованных в Налоговом кодексе РФ (далее — НК РФ), дополнен системой налогообложения в виде налога на профессиональный доход. Этот режим введен в порядке эксперимента в ряде субъектов РФ для самозанятых, зарегистрированных в органах ФНС по месту жительства в качестве плательщиков такого налога, но осуществлять свою деятельность такие граждане вправе на территории любого из субъектов Российской Федерации, включенных в эксперимент.

Вместе с тем, если человек применяет специальный налоговый режим «Налог на профессиональный доход», есть нюансы, уплаты страховых взносов, которые требуют отдельного пояснения со стороны органов ПФР.

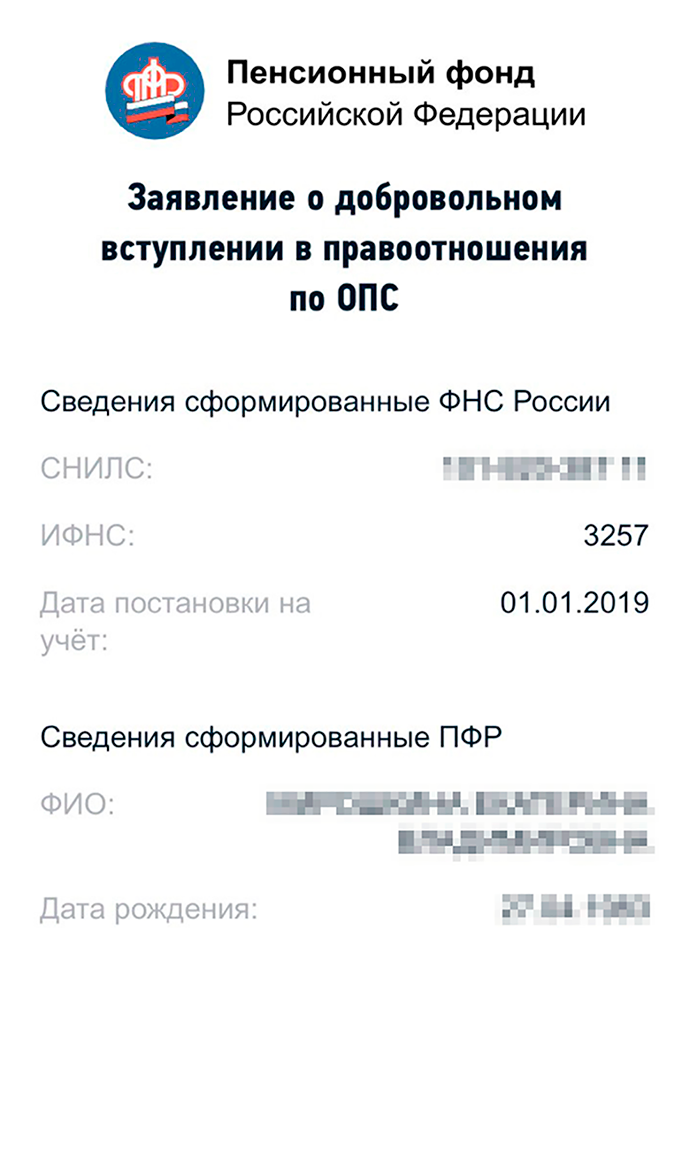

В отношении рассматриваемой категории граждан не установлена обязанность по уплате страховых взносов в ПФР. В то же время, они могут добровольно вступить в правоотношения по ОПС и уплачивать страховые взносы в порядке, определенном пунктом 5 статьи 29 Федерального закона от 15 декабря 2001 года №167-ФЗ «Об обязательном пенсионном страховании в Российской Федерации». В этом случае периоды уплаты страховых взносов засчитываются в страховой стаж таких лиц. Основанием для регистрации предпринимателя в системе ОПС является подача соответствующего заявления в органы ПФР по месту жительства.

Если физическое лицо, применяющее спецрежим «Налог на профессиональный доход», является пенсионером, и одновременно с этим добровольно уплачивает страховые взносы в рамках системы ОПС, он приобретает статус работающего пенсионера, а размер его пенсии в период осуществления такой деятельности, не индексируется.

Тем самым у лиц, применяющих режим «Налог на профессиональный доход», в период уплаты ими страховых взносов образуются пенсионные права. То есть для целей реализации пенсионных прав они считаются работающими в соответствующий временной период, что влечет правовые последствия, касающиеся выплаты пенсий и отдельных видов социальных выплат. Это определено статьей 26.1 Федерального закона от 28.12.2013 № 400-ФЗ.

Обращаем также внимание, что лица, применяющие спецрежим, могут добровольно уплачивать страховые взносы в любом размере, но не более максимального размера, определяемого как произведение 8-кратного МРОТ, установленного федеральным законом на начало финансового года, за который уплачиваются страховые взносы, и тарифа страховых взносов в ПФР, установленного пп.1 п.2 ст. 425 НК РФ, увеличенное в 12 раз. Если общая сумма уплаченных страховых взносов в течение календарного года составляет менее фиксированного размера – в страховой стаж засчитывается период, определяемый пропорционально уплаченным страховым взносам, но не более продолжительности соответствующего расчетного периода.

При подаче заявления о добровольном вступлении в правоотношения по ОПС расчетный период начинается со дня подачи заявления в территориальный орган ПФР, а заканчивается – также в день подачи соответствующего заявления в УПФР.

Группа по взаимодействию со СМИ ОПФР по Тамбовской области

«горячая линия» 79-43-99, 79-43-93

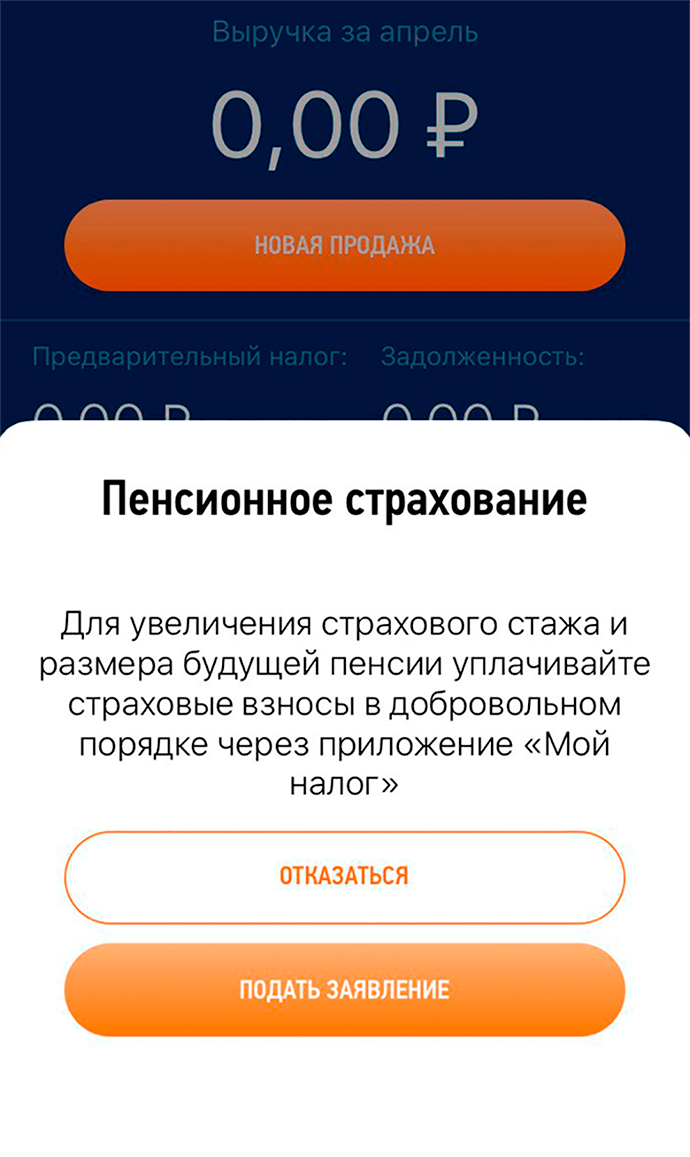

Что случилось. Самозанятые, то есть физлица и ИП, которые платят налог на профессиональный доход, могут платить взносы на свою пенсию прямо с телефона — в приложении «Мой налог». Теперь не нужно писать заявление, лично идти в пенсионный фонд или отправлять документы по почте.

Екатерина Мирошкина

экономист

О каких взносах речь. У самозанятых нет обязательных пенсионных взносов. В отличие от ИП на упрощенке, ИП на НПД может платить те же 6% налога, но страховой стаж и баллы для пенсии ему не засчитываются. У физлиц так же. Но самозанятые могут платить пенсионные взносы добровольно. Тогда у них будет идти стаж и копиться баллы, которые дадут право на пенсию по старости.

- Источник:

- ФНС

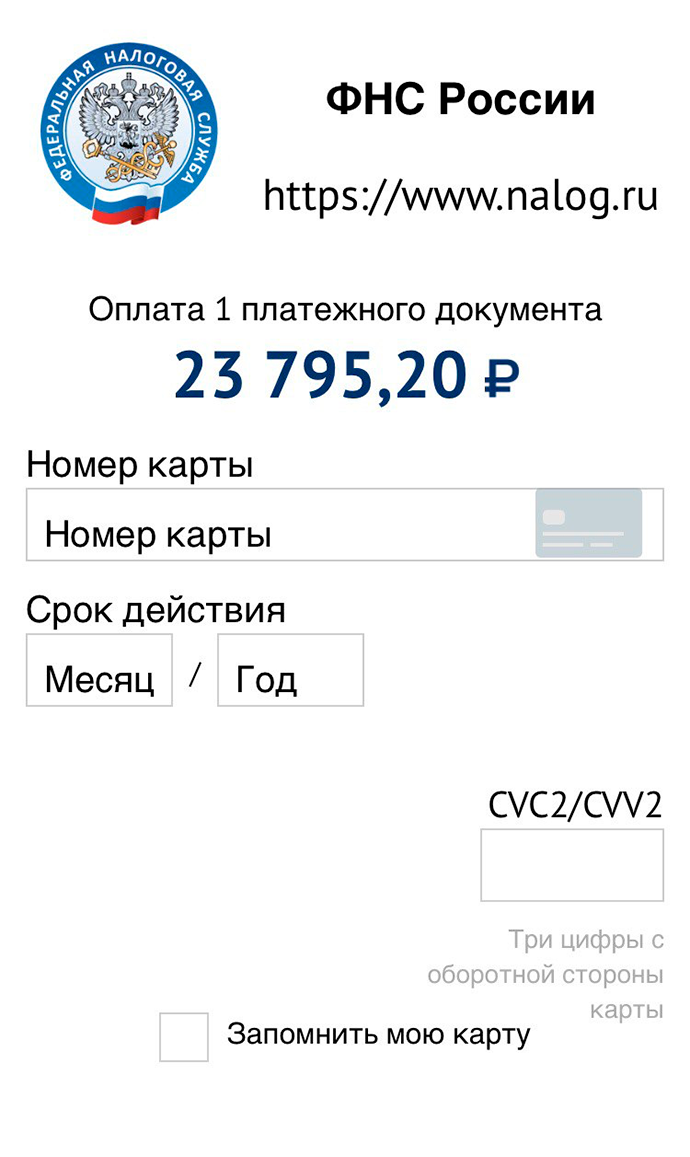

Сколько нужно платить. Чтобы засчитали полный год стажа, за 2020 год самозанятым нужно заплатить 32 448 Р. Если заплатить меньше, стаж посчитают пропорционально. Платить можно частями или сразу одной суммой. Главное — уложиться до 31 декабря текущего года.

Ну и что? 25.02.19Пенсионный стаж для самозанятых: как его купить

Как платить взносы с телефона. Взносы удобно платить через приложение «Мой налог». В личном кабинете самозанятых такой функции нет.

В приложении можно подать заявление или отказаться от добровольного страхования

В приложении можно подать заявление или отказаться от добровольного страхования Заявление сформируется и заполнится автоматически

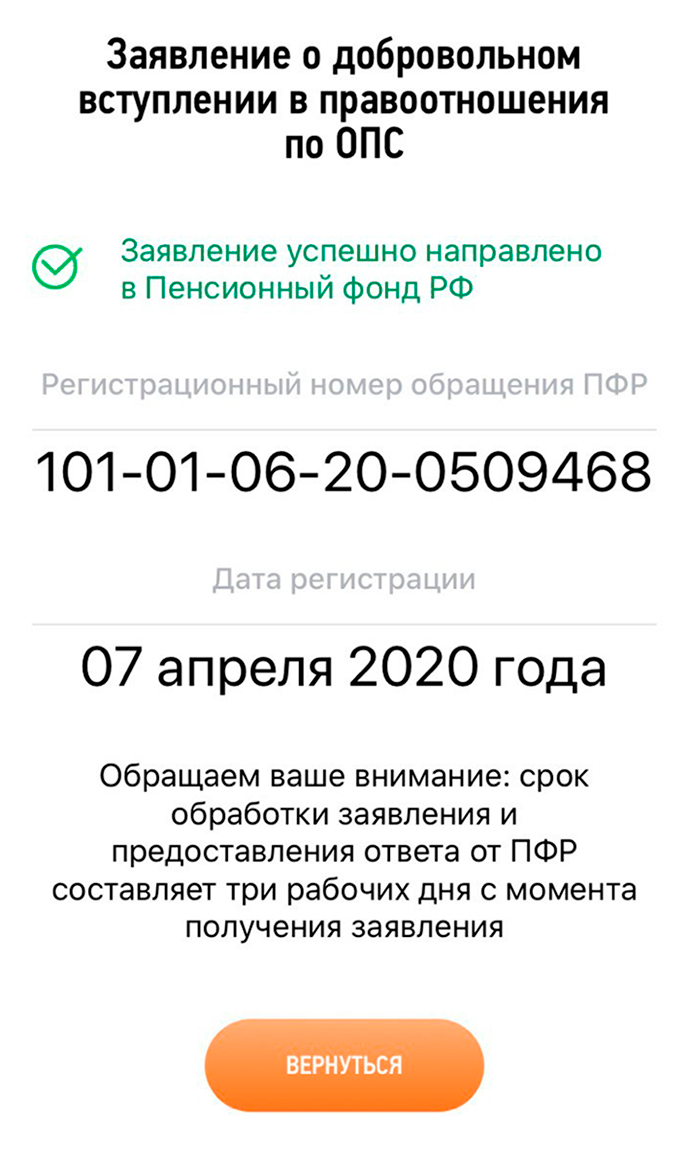

Заявление сформируется и заполнится автоматически Заявление отправляется за секунду. Больше ничего делать не нужно, только ждать: заявление будут рассматривать до трех дней. До получения ответа его нельзя отозвать

Заявление отправляется за секунду. Больше ничего делать не нужно, только ждать: заявление будут рассматривать до трех дней. До получения ответа его нельзя отозватьПосле регистрации можно будет платить добровольные взносы прямо с телефона. А можно не платить: заявление ни к чему не обязывает.

Сумма взносов рассчитывается пропорционально периоду с даты подачи заявления до конца текущего года

Сумма взносов рассчитывается пропорционально периоду с даты подачи заявления до конца текущего года Платить можно с банковской карты — сразу за весь год или любыми суммами

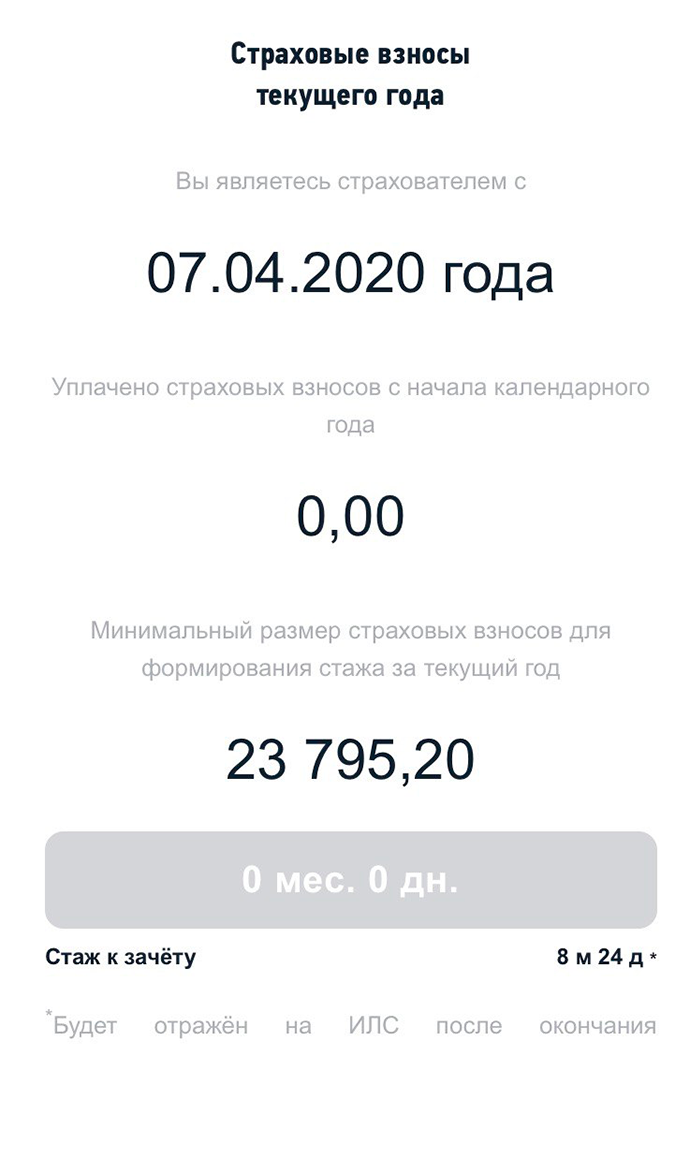

Платить можно с банковской карты — сразу за весь год или любыми суммами За 23 795 Р можно купить 8 месяцев и 24 дня стажа

За 23 795 Р можно купить 8 месяцев и 24 дня стажаКуда пойдут взносы. Взносы будут учитываться на лицевом счете. Проверить это можно по выписке — на сайте ПФР или через госуслуги. Ответ приходит моментально, услуга бесплатная. Но стаж отразится только после окончания года, за который платили взносы. Если сразу после оплаты в выписке ничего нет — это нормально.

Добровольные взносы не уменьшают налоги самозанятых

Даже если плательщик НПД — индивидуальный предприниматель, взносы на пенсионное страхование нельзя зачесть в счет налога. Если платить через «Мой налог», зачета все равно не будет. В этом плане другие режимы могут быть выгоднее. Например, на упрощенке страховые взносы уменьшают налог к уплате, а на НПД их придется платить дополнительно. Зато на НПД нет медицинских взносов: они уже входят в налог.

Не бывает идеальных налоговых режимов на все случаи жизни — всегда нужно считать.

Ну и что? 01.11.19Самозанятых пенсионеров признали неработающими. Они получат прибавку

90000 The Taxation of Foreign Pension and Annuity Distributions 90001 90002 90003 International Tax Gap Series 90004 90005 90002 A foreign pension or annuity distribution is a payment from a pension plan or retirement annuity received from a source outside the United States. You might receive it from a: 90005 90008 90009 90002 foreign employer 90005 90012 90009 90002 trust established by a foreign employer 90005 90012 90009 90002 foreign government or one of its agencies (including a foreign social security pension) 90005 90012 90009 90002 foreign insurance company 90005 90012 90009 90002 foreign trust or other foreign entity designated to pay the annuity 90005 90012 90029 90002 Just as with domestic pensions or annuities, the taxable amount generally is the Gross Distribution minus the Cost (investment in the contract).Income received from foreign pensions or annuities may be fully or partly taxable, even if you do not receive a Form 1099 or other similar document reporting the amount of the income. 90005 90002 90033 General Rule: Treaties-Pension / Annuity Articles 90034 90035 As a general rule, the pension / annuity articles of most tax treaties allow the country of residence (as determined by the residency article) to tax the pension or annuity under its domestic laws . This is true unless a treaty provision specifically amends that treatment.Some treaties, for example, provide that the country of residence may not tax amounts that would not have been taxable by the other country if you were a resident of that country. In some cases, government pensions / annuities or social security payments may be taxable by the government making the payments. There also may be special rules for lump-sum distributions. You need to look at each treaty carefully. 90005 90002 If you live in a foreign country and receive a pension / annuity paid by a U.S. payor, you may claim an exemption from withholding of U.S. Federal Income Tax (FIT) under a tax treaty by completing Form W-8BEN and delivering it to the U.S. payor. You must report your U.S. Taxpayer Identification Number (TIN) on Form W-8BEN for it to be valid for treaty purposes. 90005 90002 If you live in the USA and receive a pension / annuity paid by a payor from a foreign country, you must claim your desired treaty withholding exemption on the form, and in the manner specified by the foreign government.If the foreign government, and / or the foreign withholding agent, refuses to honor the treaty claim, make the treaty claim on your income tax return, or other prescribed form, filed with the foreign country. Additionally, you may be able to claim a Foreign Tax Credit on your U.S. federal individual income tax return for any foreign income tax withheld from your foreign pension or annuity. 90005 90002 90033 Tax Treaty Residency Issues 90034 90035 When deciding whether a tax treaty applies, identify your tax residency (Article 4 under most treaties).Then find out if the relevant treaties have articles which deal with pensions, annuities, government payments or social security payments. Remember each tax treaty is unique — just because one treaty allows a certain treatment does not mean another treaty will allow the same treatment. 90005 90002 Your residency determines how treaty articles on pensions and annuities will be applied. Use the domestic laws of each country to identify your residency, IRC 7701 (b) in the case of the USA (Green Card Test and / or Substantial Presence Test).If, after applying the domestic law of each country, you are a resident of both countries, apply the Tiebreaker Rules: 90005 90008 90009 90002 In which country do you have a 90033 Permanent Home 90034 available to you? 90005 90012 90009 90002 With which country do you have closer 90033 personal and economic relations 90034? 90005 90012 90009 90002 In which country do you have an 90033 Habitual Abode 90034? 90005 90012 90009 90002 Of which country are you a 90033 National 90034? 90005 90012 90029 90002 If none of the above tiebreaker rules works, then residency will be decided by the Competent Authorities of each country upon request by the taxpayer.Refer to Competent Authority Assistance for information on how to make a competent authority assistance request. 90005 90002 Some treaties have special rules, e.g., the USA-Canada and the USA-UK treaties have special rules for taxpayers who have U.S. green cards. You must read the residency article from beginning to end to find any special rules. You must also read all the Protocols of the treaty to see if the residency rules have been amended by a later Protocol. If you are a U.S. citizen, you also may need to refer to the so-called «saving clause» (typically found in Article 1) for special rules that allow the United States to tax in some cases as if the treaty had not entered into force.90005 90002 90033 Foreign Social Security Pensions 90034 90035 Most income tax treaties have special rules for social security payments. In many cases, foreign social security payments are taxable by the country making the payments. Unless specified otherwise in an income tax treaty, foreign social security pensions are generally taxed as if they were foreign pensions or foreign annuities. Unless a tax treaty allows it (see, e.g., the USA-Canada treaty), they are not eligible for exclusion from taxable income the way a U.S. social security pension might be. 90005 90002 90033 Foreign Employer Contributions 90034 90035 If you worked abroad, your Cost might include amounts contributed by your employer that were not includible in your gross income. This applies to contributions made either: 90005 90008 90009 90002 before 1963 by your employer for that work, 90005 90012 90009 90002 after 1962 by your employer for that work if you performed the services under a plan that existed on March 12, 1962, or 90005 90012 90009 90002 after тисяча дев’ятсот дев’яносто шість by your employer on your behalf if you were a foreign missionary (a duly ordained, commissioned, or licensed minister of a church or a lay person).90005 90012 90029 90002 90033 Foreign Contributions while a Nonresident Alien 90034 90035 Your contributions and your employer’s contributions are not part of your Cost if the contribution was based on compensation for services performed outside the United States while you were a nonresident alien and not subject to income tax under the laws of the United States or any foreign country (but only if the contribution would have been taxable if paid as cash compensation when the services were performed).90005 90002 90033 References and links: 90034 90005 90002 90005 90002 Return to: 90035 The International Tax Gap Series 90005 .90000 Pensions and Annuity Withholding | Internal Revenue Service 90001 90002 Generally, pension and annuity payments are subject to Federal income tax withholding. The withholding rules apply to the taxable part of payments from an employer pension annuity, profit-sharing, stock bonus, or other deferred compensation plan. The rules also apply to payments from an individual retirement arrangement (IRA), an annuity, endowment, or life insurance contract issued by a life insurance company. There is no withholding on any part of a distribution that is not expected to be includible in the recipient’s gross income.90003 90002 Generally, recipients of payments described above can choose not to have withholding apply to their pensions or annuities (however, refer to Mandatory Withholding on Payments Delivered Outside the United States below). The election remains in effect until the recipient revokes it. The payer must notify the recipient that this election is available. 90003 90006 Withholding on Periodic Payments 90007 90002 Generally, periodic payments are pension or annuity payments made for more than 1 year that are not eligible rollover distributions.Periodic payments include substantially equal payments made at least once a year over the life of the employee and / or beneficiaries or for 10 years or more. For wage withholding purposes, these payments are treated as if they are wages. You can figure withholding by using the recipient’s Form W-4P, Withholding Certificate for Pension or Annuity Payments, and the income tax withholding tables and methods in Publication 15, Circular E, Employer’s Tax Guide, or the alternative tables and methods in this publication.90003 90002 Recipients of periodic payments can give you a Form W-4P to specify the number of withholding allowances and any additional amount they want withheld. They may also claim exemption from withholding on Form W-4P or revoke a previously claimed exemption. If they do not submit a Form W-4P, you must figure withholding by treating a recipient as married with three withholding allowances. Refer to Form W-4P for more information. 90003 90006 Nonperiodic Payments 90007 90002 Unless you choose no withholding, the withholding rate for a nonperiodic distribution (a payment other than a periodic payment) that is not an eligible rollover distribution, is 10% of the distribution.You can also ask the payer to withhold an additional amount using Form W-4P. The part of any loan treated as a distribution (except an offset amount to repay the loan), explained later, is subject to withholding under this rule. 90003 90006 Mandatory Withholding on Payments Delivered Outside the United States 90007 90002 The election to be exempt from income tax withholding does not apply to any periodic or nonperiodic payment delivered outside the United States or its possessions to a U.S.citizen or resident alien. Refer to Form W-4P for more information. 90003 90002 A nonresident alien can elect exemption from withholding only if he or she certifies to the payer that he or she is not (1) a U.S. citizen or resident alien or (2) an individual to whom Internal Revenue Code section 877 applies (concerning expatriation to avoid tax). The certification must be made in a statement to the payer under penalties of perjury. However, nonresident aliens who choose such exemption will be subject to withholding under Internal Revenue Code section тисячі чотиреста сорок одна.Refer to Publication 515, Withholding of Tax on Nonresident Aliens and Foreign Entities, and the Instructions for Form 1042-S. Refer to NRA Withholding and Pensions, Annuities, and Alimony (Income Code 15) in Publication 515, Withholding of Tax on Nonresident Aliens and Foreign Entities. 90003 90006 Eligible Rollover Distributions 90007 90002 Withhold 20% of an eligible rollover distribution unless the recipient elected to have the distribution paid in a direct rollover to an eligible retirement plan, including an IRA.With certain exceptions, an eligible rollover distribution is the taxable part of any distribution from a qualified plan, governmental Internal Revenue Code section 457 (b) plan, tax-sheltered annuity, or IRA. For more information, refer to Chapter 8 in Publication 15-A, Employer’s Supplemental Tax Guide. 90003 90006 Depositing and Reporting Withheld Taxes 90007 90002 Report income tax withholding from pensions, annuities, and governmental Internal Revenue Code section 457 (b) plans on Form 945, Annual Return of Withheld Federal Income Tax.Do not report these liabilities on Form 941. You must furnish the recipients and the IRS with Form 1099-R, Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc. 90003 90002 Deposit withholding from pensions and annuities combined with any other nonpayroll withholding reported on Form 945 (e.g., backup withholding). Do not combine the Form 945 deposits with deposits for payroll taxes reported on Form 941 or NRA Withholding taxes reported on Form 1042.Circular E and the separate Instructions for Form 945 include information on the deposit rules for Form 945. 90003 90002 For information on withholding and reporting on pensions and annuities paid to foreign persons, refer to Pensions, Annuities, and Alimony (Income Code 15) in Publication 515, Withholding of Tax on Nonresident Aliens and Foreign Entities. 90003 90006 References / Related Topics 90007 90002 90037 90038 Note: 90039 This page contains one or more references to the Internal Revenue Code (IRC), Treasury Regulations, court cases, or other official tax guidance.References to these legal authorities are included for the convenience of those who would like to read the technical reference material. To access the applicable IRC sections, Treasury Regulations, or other official tax guidance, visit the 90040 Tax Code, Regulations, and Official Guidance 90037 page. To access any Tax Court case opinions issued after September 24, 1995, visit the 90040 Opinions Search 90037 page of the United States Tax Court. 90040 90003 .90000 Pension news: Is pension taxed? How to legally avoid paying tax on your pension 90001 90002 How much tax you pay on your pension and throughout your whole retirement varies, depending on how you choose to receive your pension. 90003 90002 While you have the option to delay receiving your pension, you may also be tempted to withdraw it all in one go. 90003 90002 But this will trigger more tax than if you were to organise annual payments or invest your funds. 90003 90002 According to The Telegraph, annual withdrawals can benefit from your personal tax-free allowance each year — and from next April this allowance will rise to £ 12,500.90003 90002 Generally, 25 per cent of a defined contribution pension — where your own contributions and your employer’s contributions are both invested — can be taken tax-free. 90003 90002 The other 75 per cent is earned as income, something many people are not aware is taxed. 90003 90002 Are there ways to reduce the amount of tax your pay on your pension legally? 90003 90002 Jonathan Watts-Lay from Wealth At Work told The Telegraph: «By making the most of allowances and reliefs, individuals can reduce or even eliminate future tax charges on their retirement income.»90003 90002 The publication gives the following scenario as an example:» Mary is eligible for the full new state pension. Together, income from her DB scheme and state pension will exceed the personal allowance, so she will be subject to some tax, but can avoid paying the maximum possible for the £ 20,000 annual income she wants. 90003 90002 «Mary has a personal allowance of £ 12,500. The £ 9,000 from her DB pension and £ 8,767 state pension give her a gross income of £ 17,767. Income tax on this would be £ 1,053, leaving a net income of £ 16,714.90003 90002 «Mary can supplement this with a £ 2,500 return from her stocks and shares ISA. She can then take £ 786 tax-free cash from her DC pension by taking her tax-free 25pc on benefits of £ 3,140, with the remaining £ 2,354 staying in her pension fund to grow. » 90003 90002 Of your pension fund, 25 per cent is tax free, and the Government website advises how you can take your tax free amount. 90003 90002 One option is to take it as a lump sum without paying tax, but you can not leave the remaining 75 per cent untouched and instead you must either buy annuity, get an adjustable income, or take the whole pot as cash.90003 90002 The other option is to receive your payments in chunks, where 25 per cent of each chunk would be tax free. 90003 90002 The government site gives the following example: «Your pot is £ 60,000 and you take £ 1,000 every month — £ 250 of this is tax free. The remaining £ 750 is taxable. » 90003 90002 Most schemes for public sector workers are defined benefit, a scheme which is agreed by the employer and guarantees a specific retirement benefit. 90003 90002 This means the amount you receive depends on the terms of the agreement, rather than how much a worker puts into their pot.90003 90002 A defined contribution scheme is based on the worker’s contributions. 90003 90002 But as a rule of thumb, Kay Ingram, director of policy at financial planners LEBC, advises you should save a percentage of salary equal to half your current age if you want to have half your salary paid as a pension by your mid 60s . 90003 90002 Speaking to Express.co.uk, she said: «So a 20 year old needs to save 10 percent a year, whereas someone starting to save at 50 would need to put aside 25 percent of earnings on a regular basis.»90003.90000 Pension Benefit Guaranty Corporation | Internal Revenue Service 90001 90002 Find resources you need to help affected individuals claim the Health Coverage Tax Credit (HCTC) or enroll in the Advance Monthly Payment (AMP) program. 90003 90002 The Health Coverage Tax Credit is a tax credit that pays 72.5 percent of qualified health insurance premiums for eligible individuals and their families. 90003 90006 Help Affected Individuals Claim the Health Coverage Tax Credit or Enroll in the 2020 Advance Monthly Payment Program 90007 90002 Individuals who qualify can choose to have 72.5 percent of qualified health insurance premiums paid monthly in advance directly to their insurance company on their behalf in 2020 to lower out-of-pocket costs for monthly premiums. 90003 90002 Individuals who choose not to get advance monthly payments and pay 100 percent of their health insurance premiums in 2020 can claim the HCTC when they file their federal tax return in 2021. 90003 90006 Help Affected Individuals Determine their Eligibility for the HCTC 90007 90002 Eligible for the HCTC if they are: 90003 90016 90017 An eligible trade adjustment assistance (TAA) recipient, alternative TAA (ATAA) recipient, or reemployment TAA (RTAA) recipient 90018 90017 An eligible Pension Benefit Guaranty Corporation payee 90018 90017 The family member of an eligible TAA, ATAA, or RTAA recipient or PBGC pension payee who is Medicare eligible, deceased, or who finalized a divorce with you.90018 90023 90002 Not eligible for the HCTC if they: 90003 90016 90017 Can be claimed as a dependent on another person’s federal income tax return; or, 90018 90017 Are enrolled in benefits under Medicare, Medicaid, the Children’s Health Insurance Program, the Federal Employees Health Benefits Program or eligible to receive benefits under the U.S. military health system. 90018 90023 90006 Ensure Health Insurance Plans Qualify for the HCTC 90007 90002 The HCTC program does not provide health coverage.Individuals will need to have or obtain qualified health coverage. Qualified HCTC plans include COBRA or spousal coverage if the employer, or former employer, did not pay 50 percent or more of the cost of coverage. Individual (private and non-group) health insurance that you purchase for yourself or your family from an insurance company, agent, or broker are also included. A qualified health plan offered through a Health Insurance Marketplace is not qualified coverage for the HCTC after December 31, 2015.90003 90002 Affected individuals should review the Instructions for Form 8885, Health Coverage Tax Credit, for information about qualified health insurance plans that are eligible for the HCTC. 90003 90006 Keep Health Insurance Records and Eligibility Documentation 90007 90002 Encourage individuals to keep the documents and records related to their eligibility to claim the credit. 90003 90016 90017 For trade certified individuals demonstrating TAA, alternative TAA, or reemployment TAA eligibility-a copy of the official letter from the Department of Labor, state workforce agency, or employment office stating they are eligible for trade adjustment benefits 90018 90017 For PBGC eligibility-a copy of the official letter from the PBGC stating they received a benefit paid by the PBGC or a copy of Form 1099-R, Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, from the PBGC showing they received a benefit paid by the PBGC 90018 90023 90002 Affected individuals should also keep copies of their proof of insurance and payment information for insurance premiums.90003 90006 Claim the HCTC 90007 90002 Eligible taxpayers can claim the HCTC for months that they met all eligibility requirements and made payments directly to a qualified health plan on their federal income tax return. They will follow special instructions and file Form 8885, 90053 Health Coverage Tax Credit (PDF) 90054, when they file their federal tax return. 90003 90006 Eligible through the Department of Labor State Workforce Agencies 90007 90058 90059 Transmission of Eligible Individuals to the IRS 90060 90061 90002 Effective January 2020 року, SWAs will identify and transmit to the IRS, via the Interstate Connection Network (ICON), the information on all individuals who meet the designation of «eligible TAA or ATAA / RTAA recipients.»ICON will remain as the communications vehicle through which states will transmit information to the IRS for HCTC purposes. 90003 90002 ICON will remain as the communications vehicle through which states will transmit information to the IRS for HCTC purposes. 90003 90006 Notices of Eligibility to Participants 90007 90002 States provide proof of eligible TAA or ATAA / RTAA recipient status to taxpayers needing such proof for submission with their tax returns. A notice of proof of eligible TAA or ATAA / RTAA recipient status must be provided separately for each year of eligibility.States need to confirm only that the individual received a payment for any one day / week in any one month during the calendar year. States may utilize the sample letter previously used during the original implementation of the HCTC. 90003 90006 Provision of Rapid Response Services 90007 90002 The provision of early and intensive Rapid Response services is vital to the success of jobseekers in obtaining timely reemployment. Rapid Response and appropriate career services must be provided to all worker groups that file a Petition for Trade Adjustment Assistance.If the petition has already been certified when the Rapid Response services are provided, information on HCTC should be provided at that time. If the Petition is still pending at the point of the initial services, additional Trade-specific sessions should be provided when the Petition is certified. 90003 90006 Eligible through the Pension Benefit Guaranty Corporation 90007 90058 90059 Transmission of Eligible Individuals to the IRS 90060 90061 90002 On the 25th of each month, PBGC will identify and transmit to the IRS, the information on all individuals who meet the designation of PBGC Payee and who is in «pay status».90003 90006 Notices of Eligibility to Participants 90007 90016 90017 PBGC uses the internet and social media to increase awareness of the HCTC program. In addition to PBGC’s HCTC webpage, its outreach efforts also include: 90016 90017 Email alerts on HCTC updates 90018 90017 Social media posts about significant HCTC updates 90018 90023 90018 90017 PBGC’s payees and people in PBGC-trusteed plans interested in the HCTC should be aware that: 90016 90017 IRS will accept a copy of Form 1099-R as proof of PBGC payee status for the year for which a taxpayer is claiming HCTC.90018 90017 If an individual wishes to enroll for the Advanced Monthly Program (AMP) they should include the most recent Form 1099-R. If an individual does not have this, they can include the trusteeship letter. 90018 90023 90018 90023 90006 Resources 90007 90002 For more information about HCTC, including frequently asked questions, eligibility and instructions, visit IRS.gov/HCTC. 90003 90002 90003 .